The AI Unlock Hiding in Plain Sight for Private Bank Lending

Private banks already have credit expertise and client relationships. The missing piece is AI that makes their advisors’ deal inputs worthy…

ReadThe intelligence to model complex UHNW credit has only ever existed inside the largest private banks. Kalynto makes it available to every advisor, family office, and lending institution — transforming complex balance sheets into structured, underwritable deals in minutes, not weeks.

Paste a Sotheby’s listing. Describe an $85M yacht acquisition. Ask about pre-IPO liquidity against concentrated stock. Lex, the platform’s AI concierge, extracts the details and starts building the deal profile in real time.

No forms. No templates. No taxonomy to learn. The platform adapts to the deal in front of it — shaping the intake around the borrower actually sitting across the table.

Every deal triggers a combination of borrower archetypes drawn from the Genome, each one adding its own stress parameters and expected document constellation to the intake.

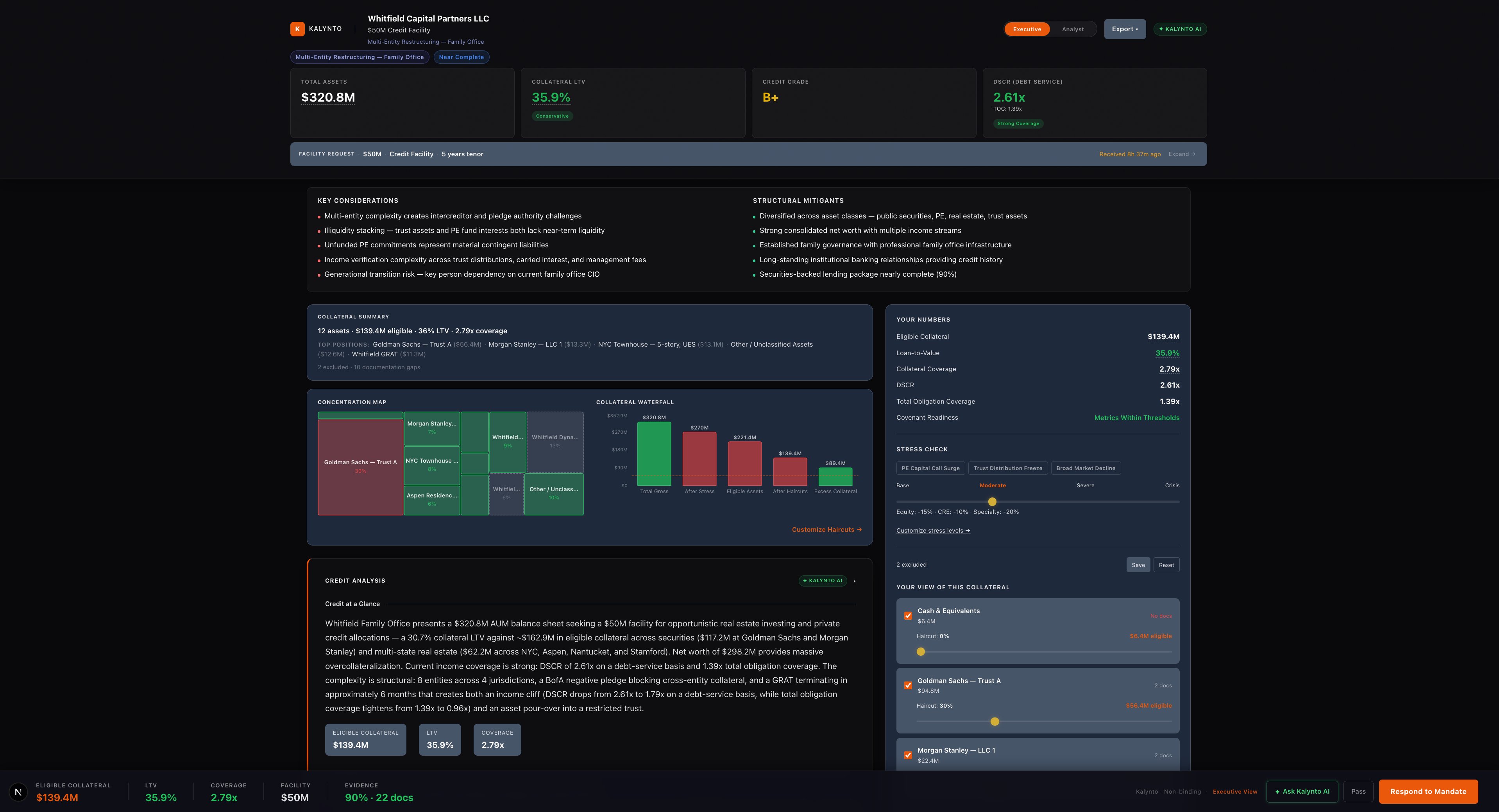

The proprietary Kalynto Genome encodes institutional credit knowledge across three layers: document understanding, borrower archetypes, and lender matching. It cross-references K-1s against trust agreements, reconciles PFS claims against brokerage evidence, detects covenant conflicts with section citations, and assembles a lender-ready dossier with full computation provenance.

Every metric traces to its source. Every red flag shows its working. The dossier is institutional-grade before it ever reaches a lender’s desk.

Every dossier includes a narrative Credit Analysis that reads like a senior underwriter. Structural risks surfaced and explained. Time-sensitive triggers identified with remediation paths. Covenant conflicts flagged with their actual section citations. A bottom line that says what this deal hinges on.

This is what the Genome compounds toward: judgment, not just data.

Every dossier exports as PDF, Excel, and PowerPoint. Institutional typography. Full provenance. Intelligence Brief. Executive Summary with grading. Structural narrative. Every number traces to its source document.

A lender drops the Excel model into Copilot, Claude, or ChatGPT and interrogates every assumption. The PDF reads like a bulge-bracket credit memo. The PowerPoint is committee-ready. Built for AI interrogation. Designed for human decisions.

After nearly two decades of building products for UHNW and institutional clients at Goldman Sachs and JPMorgan, our founder witnessed the same friction across borrowers, advisors, and lenders.

Principals and family offices with institutional-grade balance sheets were forced through slow, bespoke underwriting. Deals were lost not because the economics did not work, but because it was too hard to move high-stakes credit processes quickly and with confidence.

On the lender side, credit teams were underwriting increasingly complex mandates off of unstructured, one-off data packs: bespoke models, ad-hoc PDFs, email trails. Every mandate felt like starting from scratch.

Kalynto is that operating model: borrower dossiers with explainable signals, traceable evidence, and audit-ready selection rationales.

Private banks already have credit expertise and client relationships. The missing piece is AI that makes their advisors’ deal inputs worthy…

ReadWhy the hardest UHNW lending deals stall — and what a structured borrower package looks like when it reaches a lending desk.

ReadThe advisor tech stack covers portfolio management, planning, CRM, and compliance. Lending is nowhere. When clients need liquidity, advisors…

Read